Ben’s article was published in PEI in September 2016.

We’ve reached the turning point. Capital overhangs cause deal chasing and nosebleed auction multiples are now the standard. The off-market deal is the golden goose, yet attractive companies have little reason to shy away from sale processes. PE firms don’t want to miss out on four to six years of fees and upside as funds transition to harvest periods, so expect that capital to be put to work, one way or another.

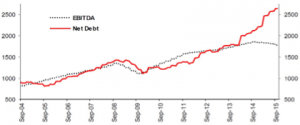

Unfortunately, business performance isn’t matching the multiple exuberance. S&P 1500 Ex-Financials EBITDA peaked at the end of 2014, yet net debt has exploded with loose credit conditions and a focus on return of capital to shareholders, rather than capex (see top chart). Rarely, if ever, have net debt and EBITDA growth diverged so dramatically – if the US economy falters, there is little room for error.

Source: SG Cross Asset Research/Equity Quant

Institutional investors are not blind – and ‘blind pool’ investing with a 10-year lock-up is losing its lustre. Larger investors are wielding the power of their capital to secure no-fee co-investment rights. Downmarket, family offices are building their own direct investment engines.

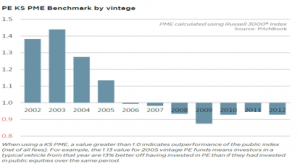

So why has the PE model worked for so long? Performance. While two and 20 is an aggressive comp model, most investors lack an alternative to access the asset class. However, following decades of outperformance against stocks, fund vintages have underperformed their public market peers since the 2006-07 market peak prior to the global financial crisis (see bottom chart).

Top performers continue to attract capital in the traditional fee model, but what about everybody else? Two and 20 looks okay with IRRs in the high teens and above, but how does it look under 10 percent? The next turn of the cycle will be punishing, especially if investors view lower returns as a new normal for the asset class. Add in benchmarking, where half of funds will lag their peers and struggle in fundraising, and you have the perfect storm.

Will this winter choke off private equity? No – just the opposite. Traditional asset classes remain in a prolonged period of uncertainty, and US demographic trends are a positive for private equity. Retiring baby boomers need buyers for their successful businesses, and private equity is a natural liquidity provider. Funds of all sizes are targeting these transitioning businesses. However, mid-market firms will feel the squeeze. Larger players are moving downmarket for platform add-ons and smaller deals, and there is rising competition from non-fund sources with deal flexibility and ways to establish working relationships beyond upfront transaction catalysts.

Successful PE investments are driven by six things: successful sourcing; efficient underwriting; selection of strong management teams; improved portfolio company operations; organic and inorganic growth realization; and interpretation of macro trends driving entry and exit points. Solid track records are a function of nailing all these, yet GP teams need not bear all the burden themselves. Top-tier firms will differentiate through competency allocation, particularly through new ways of accessing third-party sourcing channels and operational improvement expertise.

Dealflow wins. Dedicated business development professionals are now PE fixtures, something rarely seen when funds were scarce and deals aplenty. Industry and market relationships are a necessity, but another dealflow approach is growing – having others do it for you. Innovative advisory offerings and independent sponsor deals are playing a bigger role in the lower end of the market, where GPs are not set up to transact efficiently. After all, a $25 million transaction requires the same process as a $200 million one. For GPs pushing down-market, the answer is not to double or triple their bench, especially if fees are under pressure.

PE-savvy professionals are creating new models to help companies manage growth, determine optimal capitalization, and streamline PE partner selection and transaction execution. They are solving the capital readiness gap defined by murky financials, loose management processes, and a lack of information flow and systems. PE won’t fill this role, as their limited partner agreements often exclude such activities – ultimately, they’re not consulting firms. Private equity firms are holding on to their investments longer and relying more on portfolio companies’ operational improvement to drive returns. Financial engineering has its limits, banks face increasing regulation, and balance-sheet wizardry cannot be counted on as a long-term return generator.

Operational improvement is another area poorly suited to the GP. Unlike the transaction engine drawing constant bandwidth, portfolio company initiatives tend to be project-driven. The opportunity cost of using GP resources is high, while SEC oversight on expense charge-throughs adds an administrative burden.

The answer is third-party expertise. Newer consulting firms are building their value propositions specific to private equity’s needs, easing sponsor-portfolio company communication friction while focusing on tactical, value-creating solutions. Structured as a seamless extension of their own GP teams, private equity now has the tools to run lean and address the realities of longer hold periods.

The coming winter will bring about structural changes to a PE model which has held steady for a generation. While harsh seasons bring challenges, adaptation and innovation will find a way. Private equity remains a critical asset class for investment portfolios and will continue to grow – the winners recognize the threats and will leverage lean, laser-focused teams while embracing outside expertise. Funds that see just another cycle risk seeing their houses wiped from the map. Are you ready to act?

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

__hssc

30 minutes

HubSpot sets this cookie to keep track of sessions and to determine if HubSpot should increment the session number and timestamps in the __hstc cookie.

__hssrc

session

This cookie is set by Hubspot whenever it changes the session cookie. The __hssrc cookie set to 1 indicates that the user has restarted the browser, and if the cookie does not exist, it is assumed to be a new session.

cookielawinfo-checkbox-advertisement

1 year

Set by the GDPR Cookie Consent plugin, this cookie records the user consent for the cookies in the "Advertisement" category.

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

CookieLawInfoConsent

1 year

CookieYes sets this cookie to record the default button state of the corresponding category and the status of CCPA. It works only in coordination with the primary cookie.

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Cookie

Duration

Description

__cf_bm

30 minutes

Cloudflare set the cookie to support Cloudflare Bot Management.

li_gc

5 months 27 days

Linkedin set this cookie for storing visitor's consent regarding using cookies for non-essential purposes.

lidc

1 day

LinkedIn sets the lidc cookie to facilitate data center selection.

na_id

1 year 24 days

The na_id is set by AddThis to enable sharing of links on social media platforms like Facebook and Twitter.

ouid

1 year 24 days

Associated with the AddThis widget, this cookie helps users to share content across various networking and sharing forums.

UserMatchHistory

1 month

LinkedIn sets this cookie for LinkedIn Ads ID syncing.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Cookie

Duration

Description

__hstc

5 months 27 days

Hubspot set this main cookie for tracking visitors. It contains the domain, initial timestamp (first visit), last timestamp (last visit), current timestamp (this visit), and session number (increments for each subsequent session).

_fbp

3 months

Facebook sets this cookie to display advertisements when either on Facebook or on a digital platform powered by Facebook advertising after visiting the website.

_ga

1 year 1 month 4 days

Google Analytics sets this cookie to calculate visitor, session and campaign data and track site usage for the site's analytics report. The cookie stores information anonymously and assigns a randomly generated number to recognise unique visitors.

_ga_*

1 year 1 month 4 days

Google Analytics sets this cookie to store and count page views.

_gat_gtag_UA_*

1 minute

Google Analytics sets this cookie to store a unique user ID.

_gcl_au

3 months

Google Tag Manager sets the cookie to experiment advertisement efficiency of websites using their services.

_gid

1 day

Google Analytics sets this cookie to store information on how visitors use a website while also creating an analytics report of the website's performance. Some of the collected data includes the number of visitors, their source, and the pages they visit anonymously.

AnalyticsSyncHistory

1 month

Linkedin set this cookie to store information about the time a sync took place with the lms_analytics cookie.

cebs

session

Crazyegg sets this cookie to trace the current user session internally.

hubspotutk

5 months 27 days

HubSpot sets this cookie to keep track of the visitors to the website. This cookie is passed to HubSpot on form submission and used when deduplicating contacts.

ln_or

1 day

Linkedin sets this cookie to registers statistical data on users' behaviour on the website for internal analytics.

uid

1 year 24 days

This is a Google UserID cookie that tracks users across various website segments.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

Cookie

Duration

Description

__qca

1 year 26 days

The __qca cookie is associated with Quantcast. This anonymous data helps us to better understand users' needs and customize the website accordingly.

__ss

1 day

This cookie is set by SharpSpring, a marketing automation platform. This is used for tracking visitors and form submissions.

__ss_referrer

1 hour

This cookie is set by SharpSpring, a marketing automation platform. This is used for tracking visitors and form submissions.

__ss_tk

1 year 1 month 4 days

This cookie is set by SharpSpring, a marketing automation platform. This is used for tracking visitors and form submissions.

_dlt

1 day

Zendesk set this cookie to create a unique ID for the session. This enables the website to collect data on visitor behaviour for statistical purposes.

anj

3 months

AppNexus sets the anj cookie that contains data stating whether a cookie ID is synced with partners.

bcookie

1 year

LinkedIn sets this cookie from LinkedIn share buttons and ad tags to recognize browser IDs.

bscookie

1 year

LinkedIn sets this cookie to store performed actions on the website.

IDE

1 year 24 days

Google DoubleClick IDE cookies store information about how the user uses the website to present them with relevant ads according to the user profile.

koitk

1 year 1 month 4 days

This cookie is set by SharpSpring, a marketing automation platform. This is used for tracking visitors and form submissions.

li_sugr

3 months

LinkedIn sets this cookie to collect user behaviour data to optimise the website and make advertisements on the website more relevant.

mc

1 year 1 month

Quantserve sets the mc cookie to track user behaviour on the website anonymously.

muc_ads

1 year 1 month 4 days

Twitter sets this cookie to collect user behaviour and interaction data to optimize the website.

pa_crosswise_ts

1 year 1 month 4 days

Perfect Audience sets this cookie to collect information in a way that does not directly identify anyone, including the number of visitors to the website and blog.

pa_google_ts

1 year 1 month 4 days

Perfect Audience sets this cookie to collect information about how visitors use the website.

pa_openx_ts

1 year 1 month 4 days

Perfect Audience sets this cookie to collect information in a way that does not directly identify anyone, including the number of visitors to the website and blog.

pa_rubicon_ts

1 year 1 month 4 days

Perfect Audience sets this cookie to collect information about how visitors use the website.

pa_twitter_ts

1 year 1 month 4 days

Perfect Audience sets this cookie to collect information about how visitors use the website.

pa_uid

1 year 1 month 4 days

Perfect Audience sets this cookie for advertising purposes based on user behaviour data.

pa_yahoo_ts

1 year 1 month 4 days

Perfect Audience sets this cookie to collect information in a way that does not directly identify anyone, including the number of visitors to the website and blog.

personalization_id

1 year 1 month 4 days

Twitter sets this cookie to integrate and share features for social media and also store information about how the user uses the website, for tracking and targeting.

test_cookie

15 minutes

doubleclick.net sets this cookie to determine if the user's browser supports cookies.

uuid2

3 months

The uuid2 cookie is set by AppNexus and records information that helps differentiate between devices and browsers. This information is used to pick out ads delivered by the platform and assess the ad performance and its attribute payment.